You've made it this far by making the right decisions.

Our tailored investment strategies can provide income generation, inflation protection, and growth to meet your lifestyle needs.

“Tyson Halsey of Income Growth Advisors has been managing separately managed accounts made up of master limited partnerships for 15 years. He has weathered the ups and downs of the past two years to boast a 77% one-year return and a 1.7% three-year return, (including a 5% dip in February), in his latest letter to shareholders.”

– Amey Stone, Barron’s

Bespoke Portfolios for Where You Are,

and Where You're Going.

What Separates IGA?

Experience and tailored investment strategies are what separate IGA from its competition. Since 1984, Halsey has worked on Wall Street and has distinguished himself repeatedly. Halsey worked on the floor of the New York Futures Exchange and in brokerage at Merrill Lynch, Alex. Brown, and Deutsche Bank. He won the USA Today CNBC National Investment Challenge in 1992 and was conferred the CFA designation in 1993. Halsey founded two investment advisories and three hedge funds.

Halsey’s trading, equity analysis, and portfolio management experience form the backbone of IGA and keep him connected with network of renowned and talented investment professionals with whom he confers.

Halsey has been cited in Barron’s and the Wall Street Journal. Halsey publishes regularly on Seeking Alpha, twice selected as SA’s Editor’s Choice, appears on South Carolina Public Radio, CNBC and posts on social media.

Why Commodities Now?

Markets go through cycles. Today’s investment environment has radically shifted to an inflationary commodity super cycle. Inflation is now matching 40-year high levels and interest rates are rising. Forty years of declining interest rates have now reversed, and this environment is threatening bubbles in stocks, bonds, and real estate. Many of the stocks and strategies which have worked so well for investors for the last 40 and or 10 years won’t offer the same high returns they have grown to expect.

Consequently, IGA is investing in securities with portfolio strategies that should perform well in this new market environment.

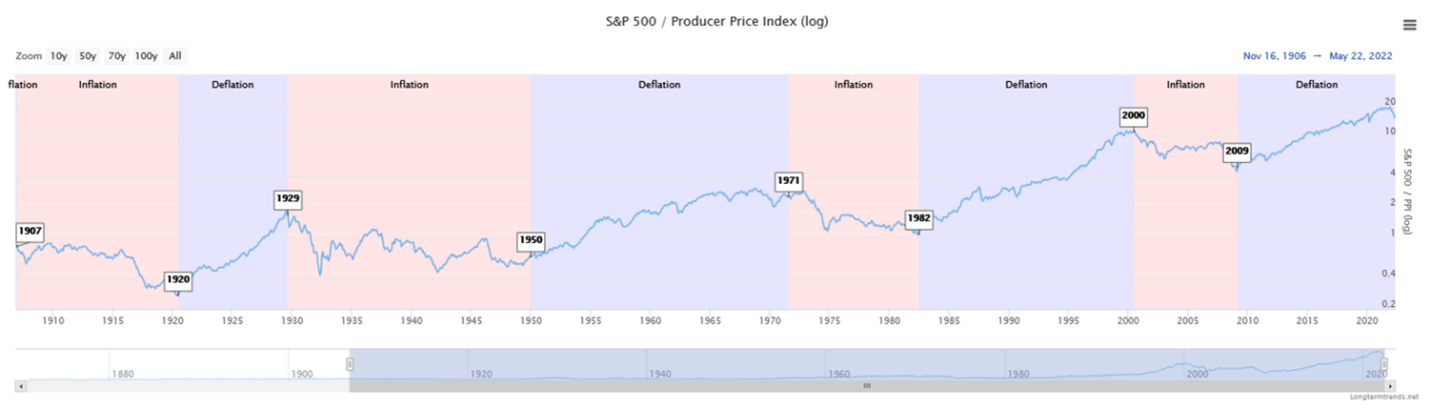

There is no simple formula to investing; however, our current client portfolios emphasize commodities, precious metals, energy, Master Limited Partnerships, and inflation-beneficiaries. Since the COVID-19 market bottom, our client portfolios are up nicely and outperforming while most major stock indices and bonds are having historically terrible performance. We attribute our recent success to recognizing the fundamental and economic factor changes of today’s inflationary commodity super cycle. See the inflationary deflationary cycle chart below:

Account Types

Income Growth Advisors, LLC offers two principal ways to invest. We can manage your investment account, 401-K, 529, or retirement account at your existing custodian. Without having to move your account, Income Growth Advisors, LLC can select mutual funds and securities that institution offers to easily manage your portfolio. Through Pontera, formerly Fee-X, we can invest your account on your current platform on a fee basis.

We also manage discretionary accounts and non-discretionary accounts through Interactive Brokers LLC. Those accounts can be individual accounts, retirement accounts, or college savings accounts including IRA Rollovers, SEPs, 401Ks, 529s, Inherited IRAs, Roth IRAs, and traditional IRAs. In every situation, we discuss with you what your investment objectives are and craft a program to meet your goals and objectives.

Interactive Brokers is an American multinational brokerage firm that offers low-cost commissions and margin rates. It operates the largest electronic trading platform in the U.S.

“Unfortunately, most people who buy [royalty trusts] don’t realize that they tend to be depleting assets,” says Tyson Halsey of Income Growth Advisors, an investment firm in Charleston, S.C. “They end up being bad for retired people who think they are getting a fixed-income alternative.”

The Intelligent Investor Column, Jason Zweig, Wall Street Journal

Your Existing Institution, Our Time-Tested Expertise.

Income Growth Advisors, LLC through Pontera (formerly FeeX) can manage your retirement assets, college savings and other assets at any of these leading financial institutions.

We can manage, monitor and rebalance your employer-sponsored retirement accounts, including 401k and 403b.

Let us take care of your 401k with a personalized strategy and manage your assets right where they are through Pontera.

Subscribe to Our Newsletter

Income Growth Advisors, LLC publishes its monthly newsletter on Seeking Alpha and our letter has been selected as “Editor’s Choice”. Seeking Alpha costs $299.99/month. Our newsletter is free.